Have you ever set your utility bill to auto-pay? Split a dinner bill by sending your friend cash through Venmo? Had the IRS drop a nice, juicy tax refund straight into your checking account? If so, you’ve already experienced the benefits of ACH payment.

And you’re definitely not alone. In fact, 2021 saw 29.1 billion ACH payments covering $72.6 trillion of value, according to data from Nacha. That works out to around 87 transactions for every person in America. ACH payments touch our lives in so many ways that customers now expect the convenience that they offer. That’s good news for you because ACH payments can also save your business money and reduce the risk of fraud. ACH also makes it easy to offer subscriptions and recurring payments– freeing up time for both your customers and sales team.

What is ACH payment?

An ACH payment is a type of electronic transaction that transfers money from bank to bank.

ACH stands for “Automated Clearing House”, which is a network that connects all banks within the United States. This connection allows the transfer of money directly between banks, without relying on paper checks, wire transfers, or credit card processing.

The clearinghouse is maintained and governed by an organization called Nacha (formerly NACHA or the National Automated Clearing House Association). Nacha also sets the rules and regulations that protect your and your customers.

Some common examples of ACH payments include:

- PayPal or Venmo

- Direct deposit payroll

- Direct deposit tax refunds

- Automatic bill pay

ACH isn’t the only type of electronic payment though, so it can get confused with other payment methods. Let’s take a look at a few common questions you may have.

Is ACH payment the same as EFT?

EFT, or electronic funds transfer, is a catch-all term for any type of digital payment. An ACH payment is one type of EFT, but there are many other types, including credit cards, ATMs, and wire transfers.

Is ACH payment the same as wire transfer?

Wire transfers and ACH payments are both examples of electronic transactions, but they’re not the same.

The biggest difference is that wire transfers are individual requests that happen in real-time. ACH transactions are processed in batches at set times throughout the day. This means that funds from wire transfers are often available on the same day, while ACH payments may take up to 3-5 business days to complete.

That high speed comes with a high price tag though. The second biggest difference is that wire transfers average around $25 per transaction. Compare that to the average ACH fee of around $0.29.

The last important difference is that ACH payments are reversible, while wire transfers are permanent.

| Wire Transfer | ACH Payment | |

| Cadence | Real-time | Batched |

| Timeline | Same day | 3-5 bus. days |

| Avg. Cost | $25 | $0.29 |

| Reversible? | No | Yes |

Types of ACH Payment

There are two kinds of ACH payments: credit and debit. The difference between them is in which direction the transaction goes.

ACH Credit – Used by a business to “push” money into another bank account.

Example: Direct deposit paychecks.

ACH Debit – Used by a business to “pull” money from a customer’s bank account.

Example: Auto bill pay

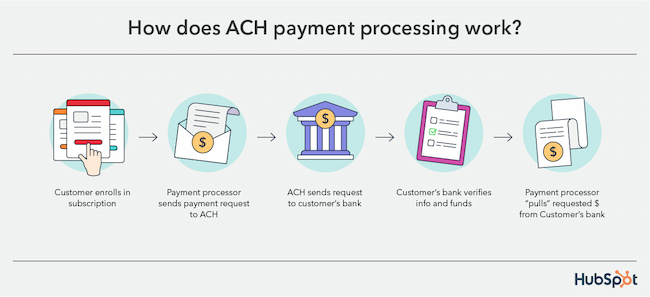

A Closer Look at an ACH Payment

To better understand how ACH payment processing works, let’s take an example of an ACH debit.

- Your customer enrolls in a monthly subscription. They give you their bank account information and payment authorization.

- When payment is due, your payment processor sends a request to the clearinghouse. (In Nacha terms your processor is the Originating Depository Financial Institution or ODFI.)

- The clearinghouse processes that request as part of a batch of requests and then sends it to your customer’s bank. (Your customer’s bank is the Receiving Depository Financial Institution or RDFI.)

- Your customer’s bank receives the request and verifies that your customer’s information is accurate. And that they have enough money to cover the bill.

- If everything checks out, your customer’s bank (the RDFI) allows your processor (the ODFI) to “pull” the requested funds.

An ACH credit works the same way, except that the ODFI “pushes” the money to the RDFI instead.

Some ACH payments may be eligible for same-day, next-day, or 2-day processing, but this will bump up the cost.

Is ACH payment safe?

According to a study done by the Federal Reserve, ACH payments have the lowest rate of fraud by value, averaging only $0.08 of fraud for every $10,000. That makes ACH more secure than credit cards, debit cards, or even ATM withdrawals.

That’s because Nacha has strict rules and guidelines for risk management. These rules require all banks or businesses involved to take “commercially reasonable” steps to verify customer information and protect sensitive data.

That said, “reasonable” can mean different things for different businesses. It’s important to make sure that your payment processor uses up-to-date security measures.

For example, HubSpot payments ensures all payment credentials are both encrypted and tokenized. By using multiple layers of security, your customers can trust that you’re keeping their sensitive information protected.

How much does ACH payment cost?

Nacha doesn’t set the fees associated with ACH payments, so the cost depends on the bank or payment processor you use.

Some processors charge a flat fee, which typically ranges from $0.20 to $1.50 per transaction. Others may charge a percentage of the transaction amount, and this generally falls between 0.5% to 1.5%.

Third-party processors may also charge extra fees upfront or monthly to use their service, so make sure you’re comparing all costs when choosing a provider.

With HubSpot payments, you pay 0.5% of the transaction amount, with a cap of $10 per transaction. There are no monthly fees, setup costs, or hidden charges, so you only ever pay for the service when you need it.

Is ACH payment right for your business?

Whether ACH is right for you comes down to the needs of your business. A company that relies on monthly billing can save a lot of money by using ACH instead of credit cards. On the other hand, ACH may not make sense for a retailer without a lot of repeat customers.

Here are a few reasons you might use – or not use – ACH payments.

When to Use ACH

- Your business involves recurring payments or subscriptions.Accepting ACH payments means your customers don’t have to remember to dig out their wallets every month.

- You’re tired of sending paper invoices. ACH payments are handled entirely online. In fact, HubSpot payments allows you to accept payment straight from your own website. Or create secure, shareable payment links that your customers can access by phone, email, or even online chat.

- You need to save on credit card fees. Credit card processing fees often run 2-3% or more.

- Your customers’ payments are getting declined. ACH payments come directly from your customers’ bank accounts. This means fewer rejected payments than credit cards, which can expire or get lost or stolen.

- Your customers’ security is a top priority. ACH payments experience less fraud than any other payment processing method.

When to Not Use ACH

- You have a lot of international customers. Although ACH will still work great for customers in the U.S. or U.S. territories.

- Your customers need to make high-dollar payments.Although Nacha has raised the per-transaction limit to $100,000, your bank or payment processor may impose their own limits.

- You can’t wait 3-5 business days for payment. ACH payments are slower than credit card processing or wire transfer.

How to Accept ACH Payment

If you want to start accepting ACH payments regularly, you’ll want to work with a third-party payment processor. While you can handle ACH transactions through your bank, they likely won’t offer you a secure method of collecting your customers’ account information.

Sales Hub users can sign up for ACH transactions in minutes, and typically start accepting payments within 1-2 business days.

And HubSpot payments integrates directly with your CRM, so your customers can make secure payments straight through your website, email, or online chat. Or put secure, shareable links right into your quotes.

Leveraging ACH Payments for Your Business

Of course, choosing ACH payments isn’t an either-or decision. Many payment processors, including HubSpot, allow you to accept ACH and credit cards from the same tool. Offering your customers multiple payment options makes it easier for them to make a purchase. And that means more money in your bank.

![]()

![Read more about the article 7 Habits of Highly Effective People [Summary & Takeaways]](https://www.dimaservices.agency/wp-content/uploads/2022/04/5ab914ce-204e-40ef-acfe-d7bfec642e1a-300x26.png)